Interest Rate Models

Interest rate models are defined as a list of governance-approved contracts. Each contract implements the IRM interface exposed below.

Function

borrowRate

function borrowRate(MarketParams memory marketParams, Market memory market) external returns (uint256);

Returns the borrow rate of the market marketParams.

Parameters:

| Name | Type | Description |

|---|---|---|

marketParams | MarketParams | The MarketParams struct of the market. |

market | Market | The Market struct of the market. |

Return values:

| Name | Type | Description |

|---|---|---|

borrowRate | uint256 | The borrow rate of the market. |

View Function

borrowRateView:

function borrowRateView(MarketParams memory marketParams, Market memory market) external view returns (uint256);

Returns the borrow rate of the market marketParams without modifying any storage.

Parameters:

| Name | Type | Description |

|---|---|---|

marketParams | MarketParams | The MarketParams struct of the market. |

market | Market | The Market struct of the market. |

Return values:

| Name | Type | Description |

|---|---|---|

borrowRate | uint256 | The borrow rate of the market. |

Calculations

The Annual Percentage Yields (APY) for both borrowing and supplying are key indicators of the returns for lenders and the cost for borrowers. The APY takes into account the compounding interest to provide a standardized measure of yields over a one-year period.

Borrow APY

The Borrow APY is calculated using the following formula:

Where:

borrowRateis the borrow rate per second, as determined by the Interest Rate Model (IRM),secondsPerYearrepresents the total number of seconds in a year (31,536,000).

To obtain the borrowRate value, a simple call can be made to the borrowRateView or borrowRate functions defined in the upper sections.

Supply APY

The Supply APY is calculated considering the utilization and the fee. The formula is:

Where:

feeis the fee of the market, to be activated by the DAO, on a per-market basis,utilizationis calculated as:

Manual retrieval of the borrow rate:

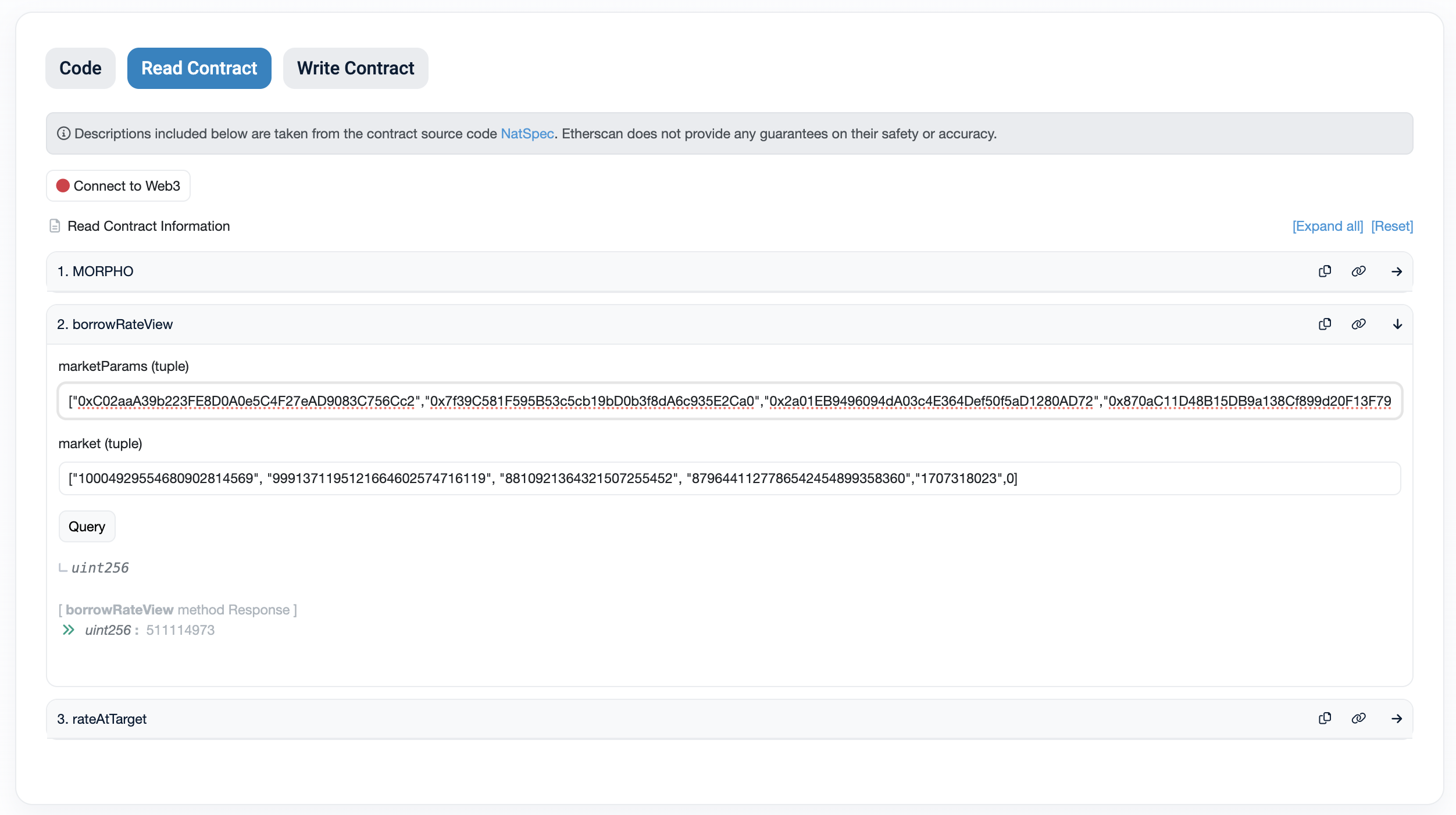

To manually retrieve the borrowRate for a market, you can use the borrowRateView function of the IRM contract. This section guides you through the process of obtaining the necessary parameters and executing the function call.

Jump into the Addresses section to get the contract addresses.

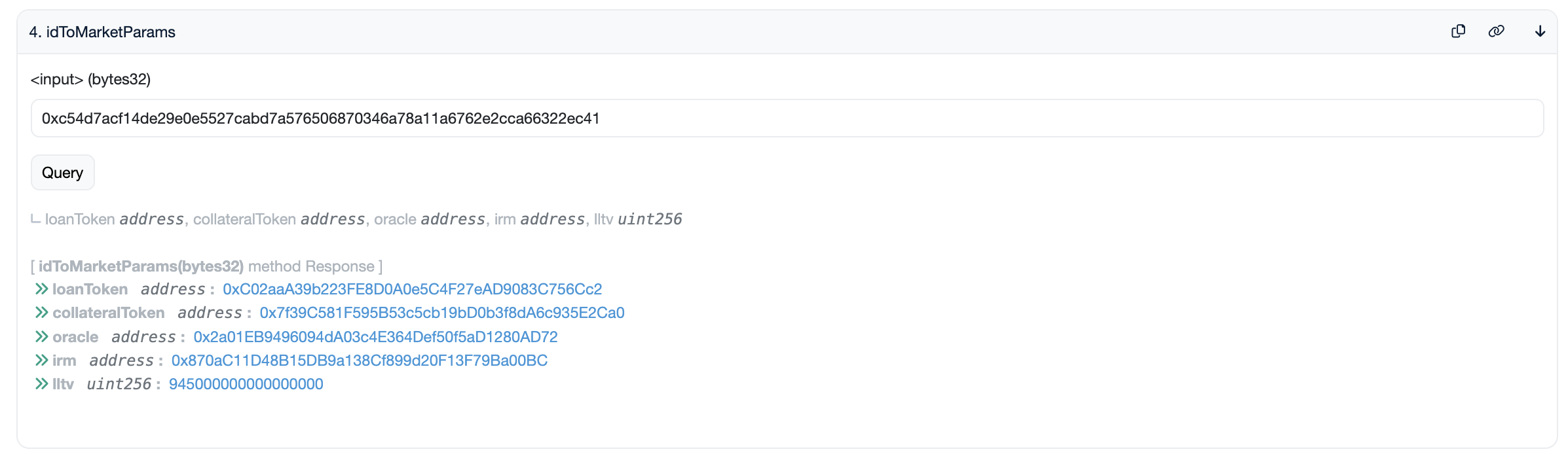

- Querying the Morpho Blue Contract

First, obtain the marketParams by querying the idToMarketParams function. For example, for the wstETH/WETH (94.5%) market, use the following ID: 0xc54d7acf14de29e0e5527cabd7a576506870346a78a11a6762e2cca66322ec41.

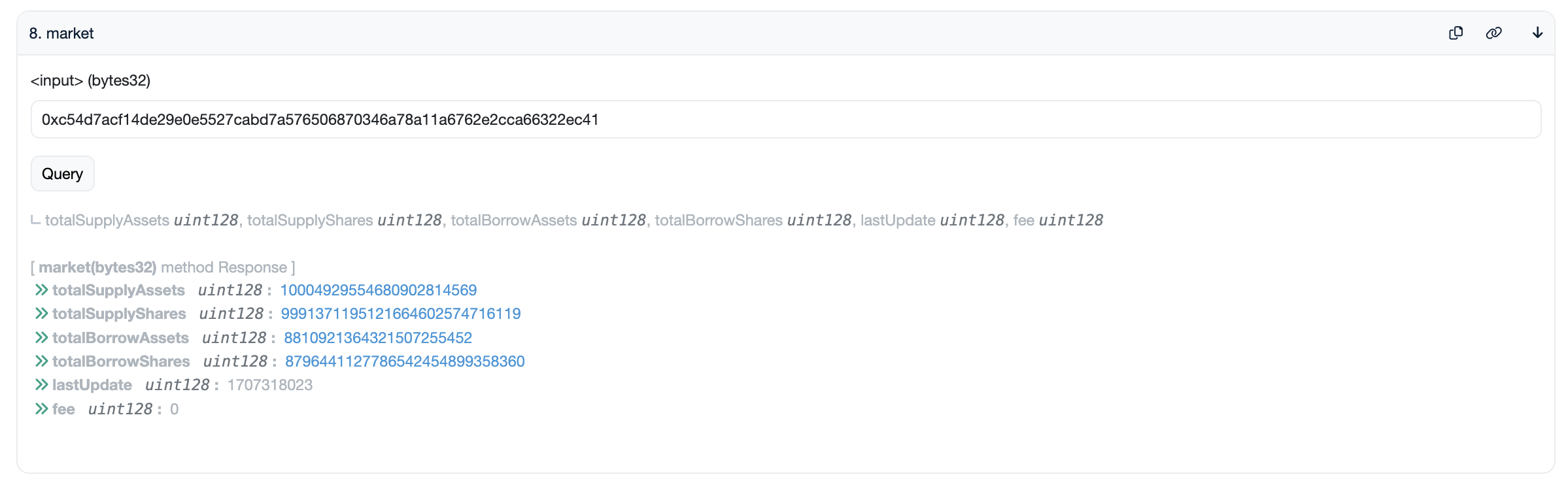

Next, acquire the market values by querying the market function.

- Querying the AdaptiveCurveIRM Contract

Use the retrieved marketParams and market in the following format to query the contract:

Input:

marketParams(tuple)

["0xC02aaA39b223FE8D0A0e5C4F27eAD9083C756Cc2","0x7f39C581F595B53c5cb19bD0b3f8dA6c935E2Ca0","0x2a01EB9496094dA03c4E364Def50f5aD1280AD72","0x870aC11D48B15DB9a138Cf899d20F13F79Ba00BC","945000000000000000"]

market(tuple)

["10004929554680902814569", "9991371195121664602574716119", "8810921364321507255452", "8796441127786542454899358360","1707318023",0]